Why are commodity prices, including oil prices, lagging? Ultimately, the question comes back to, “Why isn’t the world economy making very many of the end products that use these commodities?” If

workers were getting rich enough to buy new homes and cars, demand for

these products would be raising the prices of commodities used to build

and operate cars, including the price of oil. If governments were rich

enough to build an increasing number of roads and more public housing,

there would be demand for the commodities used to build roads and public

housing.

It looks to me as though we are heading into a

deflationary depression, because the prices of commodities are falling

below the cost of extraction. We need rapidly rising wages and debt if

commodity prices are to rise back to 2011 levels or higher. This isn’t

happening. Instead, Janet Yellen is talking about raising interest rates

later this year, and we are seeing commodity prices fall further and further. Let me explain some pieces of what is happening.

1.

We have been forcing economic growth upward since 1981 through the use

of falling interest rates. Interest rates are now so low that it is hard

to force rates down further, in order to encourage further economic

growth. Falling interest rates are hugely beneficial for

the economy. If interest rates stop dropping, or worse yet, begin to

rise, we will lose this very beneficial factor affecting the economy.

The economy will tend to grow even less quickly, bringing down commodity

prices further. The world economy may even start contracting, as it

heads into a deflationary depression.

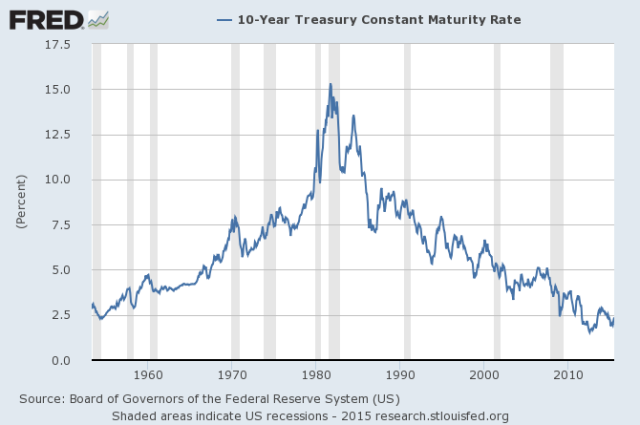

If we look at 10-year US treasury interest rates, there has been a steep fall in rates since 1981.

Figure 1. Chart prepared by St. Louis Fed using data through July 20, 2015.

In

fact, almost any kind of interest rates, including interest rates of

shorter terms, mortgage interest rates, bank prime loan rates, and

Moody’s Seasoned AAA Bonds, show a fairly similar pattern. There is more

variability in very short-term interest rates, but the general

direction has been down, to the point where interest rates can drop no

further.

Declining interest rates stimulate the economy for many reasons:

- Would-be homeowners find monthly payments are lower, so more people can afford to purchase homes. People already owning homes can afford to “move up” to more expensive homes.

- Would-be auto owners find monthly payments lower, so more people can afford cars.

- Employment in the home and auto industries is stimulated, as is employment in home furnishing industries.

- Employment at colleges and universities grows, as lower interest rates encourage more students to borrow money to attend college.

- With lower interest rates, businesses can afford to build factories and stores, even when the anticipated rate of return is not very high. The higher demand for autos, homes, home furnishing, and colleges adds to the success of businesses.

- The low interest rates tend to raise asset prices, including prices of stocks, bonds, homes and farmland, making people feel richer.

- If housing prices rise sufficiently, homeowners can refinance their mortgages, often at a lower interest rate. With the funds from refinancing, they can remodel, or buy a car, or take a vacation.

- With low interest rates, the total amount that can be borrowed without interest payments becoming a huge burden rises greatly. This is especially important for governments, since they tend to borrow endlessly, without collateral for their loans.

While

this very favorable trend in interest rates has been occurring for

years, we don’t know precisely how much impact this stimulus is having

on the economy. Instead, the situation is the “new normal.” In some

ways, the benefit is like traveling down a hill on a skateboard, and not

realizing how much the slope of the hill is affecting the speed of the

skateboard. The situation goes on for so long that no one notices the

benefit it confers.

If the economy is now moving too slowly, what

do we expect to happen when interest rates start rising? Even level

interest rates become a problem, if we have become accustomed to the

economic boost we get from falling interest rates.

2.

The cost of oil extraction tends to rise over time because the cheapest

to extract oil is removed first. In fact, this is true for nearly all

commodities, including metals.

If costs always remained

the same, we could represent the production of a barrel of oil, or a

pound of metal, using the following diagram.

Figure 2. Base Case

If

production is becoming increasingly efficient, then we might represent

the situation as follows, where the larger size “box” represents the

larger output, using the same inputs.

Figure 3. Increased Efficiency

For

oil and for many other commodities, we are experiencing the opposite

situation. Instead of becoming increasingly efficient, we are becoming

increasingly inefficient (Figure 4). This happens because deeper wells

need to be dug, or because we need to use fracking equipment and

fracking sand, or because we need to build special refineries to handle

the pollution problems of a particular kind of oil. Thus we need more

resources to produce the same amount of oil.

Figure 4. Growing inefficiency (Notice how sizes of shapes differ in Figures 2, 3, and 4.)

Some people might call the situation “diminishing returns,”

because the cheap oil has already been extracted, and we need to move

on to the more difficult to extract oil. This adds extra steps, and thus

extra costs. I have chosen to use the slightly broader term of

“increasing inefficiency” because it indicates that the nature of these

additional costs is not being restricted.

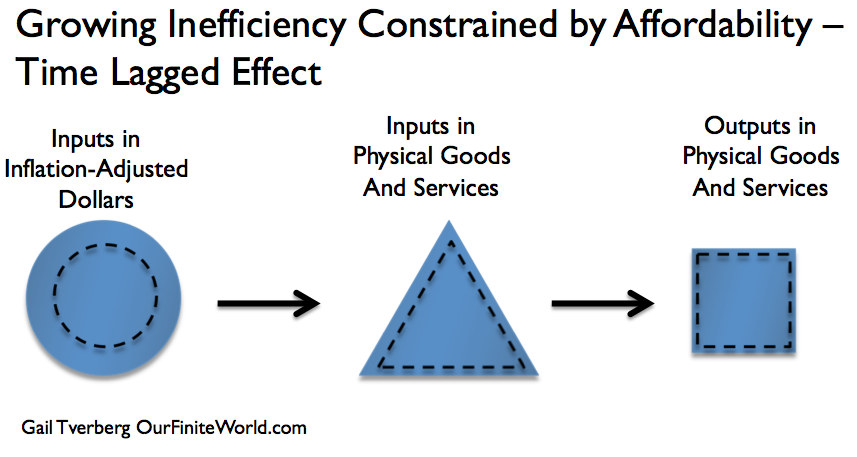

Very often, new steps

need to be added to the process of extraction because wells are deeper,

or because refining requires the removal of more pollutants. At times,

the higher costs involve changing to a new process that is believed to

be more environmentally sound.

Figure

5. An example of what may happen to make inputs in physical goods and

services rise. (The triangle shape was chosen to match the shape of the

“Inputs of Goods and Services” triangle in Figures 2, 3, and 4.)

The

cost of extraction keeps rising, as the cheapest to extract resources

become depleted, and as environmental pollution becomes more of a

problem.

3. Using more inputs to create the same or smaller output pushes the world economy toward contraction.

Essentially,

the problem is that the same quantity of inputs is yielding less and

less of the desired final product. For a given quantity of inputs, we

are getting more and more intermediate products (such as fracking sand, “scrubbers”

for coal-fired power plants, desalination plants for fresh water, and

administrators for colleges), but we are not getting as much output in

the traditional sense, such as barrels of oil, kilowatts of electricity,

gallons of fresh water, or educated young people, ready to join the

work force.

We don’t have unlimited inputs. As more and more of

our inputs are assigned to creating intermediate products to work around

limits we are reaching (including pollution limits), fewer of our

resources can go toward producing desired end products. The result is

less economic growth. Because of this declining economic growth, there

is less demand for commodities. So, prices for commodities tend to drop. This outcome is to be expected, if increased efficiency is part of what creates economic growth, and what we are experiencing now is the opposite: increased inefficiency.

4.

The way workers afford higher commodity costs is primarily through

higher wages. At times, higher debt can also be a workaround. If neither

of these is available, commodity prices can fall below the cost of

production.

If there is a significant increase in the

cost of products like houses and cars, this presents a huge challenge to

workers. Usually, workers pay for these products using a combination of

wages and debt. If costs rise, they either need higher wages, or a debt

package that makes the product more affordable–perhaps lower rates, or a

longer period for payment.

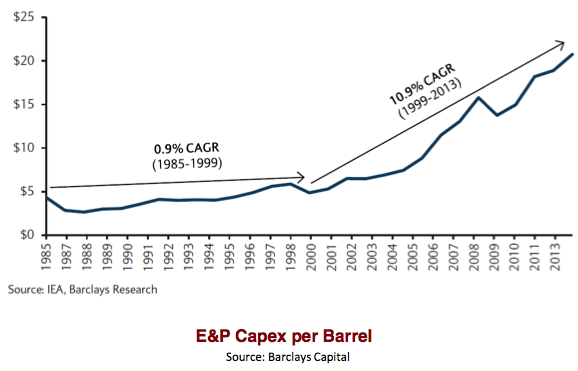

Commodity costs have been rising very rapidly in the last fifteen years or so. According to a chart prepared by Steven Kopits, some of the major costs of extracting oil began increasing by 10.9% per

year, in about 1999.

Figure

6. Figure by Steve Kopits of Westwood Douglas showing trends in world

oil exploration and production costs per barrel. CAGR is “Compound

Annual Growth Rate.”

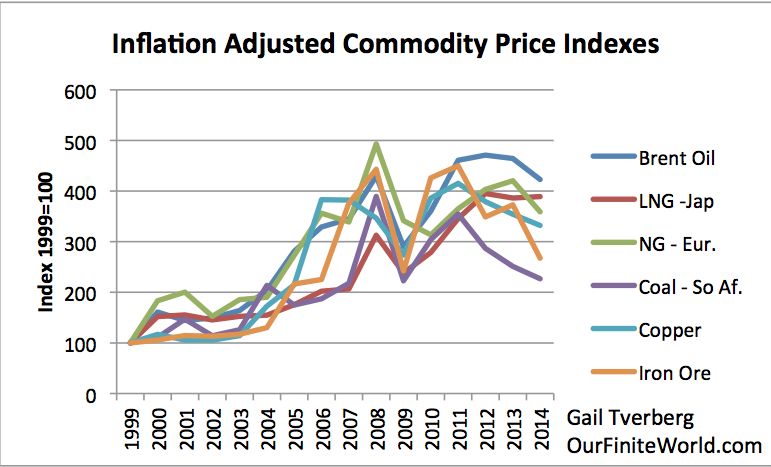

In fact, the inflation-adjusted prices

of almost all energy and metal products tended to rise rapidly during

the period 1999 to 2008 (Figure 7). This was a time period when the amount

of mortgage debt was increasing rapidly as lenders began offering home

loans with low initial interest rates to almost anyone, including

those with low credit scores and irregular income. When debt levels

began falling in mid-2008 (related in part to defaulting home loans),

commodity prices of all types dropped.

Figure 6. Inflation adjusted prices adjusted to 1999 price = 100, based on World Bank “Pink Sheet” data.

Prices

then began to rise once Quantitative Easing (QE) was initiated (compare

Figures 6 and 7). The use of QE brought down medium-term and long-term

interest rates, making it easier for customers to afford homes and cars.

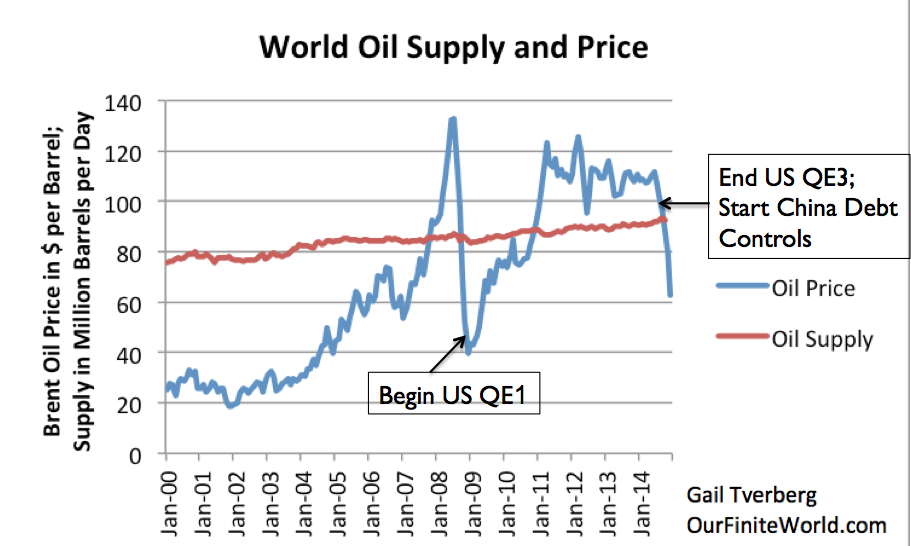

Figure

7. World Oil Supply (production including biofuels, natural gas

liquids) and Brent monthly average spot prices, based on EIA data.

More

recently, prices have fallen again. Thus, we have had two recent times

when prices have fallen below the cost of production for many major

commodities. Both of these drops occurred after prices had been high,

when debt availability was contracting or failing to rise as much as in

the past.

5. Part of the problem that we are experiencing is a slow-down in wage growth.

Figure

8 shows that in the United States, growth in per capita wages tends to

disappear when oil prices rise above $40 barrel. (Of course, as noted in

Point 1, interest rates have been falling since 1981. If it weren’t for

this, the cut off for wage growth might even be lower–perhaps even $20

barrel!)

Figure

8. Average wages in 2012$ compared to Brent oil price, also in 2012$.

Average wages are total wages based on BEA data adjusted by the

CPI-Urban, divided by total population. Thus, they reflect changes in

the proportion of population employed as well as wage levels.

There

is also a logical reason why we should expect that wages would tend to

fall as energy costs rise. How does a manufacturer respond to the much

higher cost of one or more of its major inputs? If the manufacturer

simply passes the higher cost along, many customers will no longer be

able to afford the manufacturer’s or service-provider’s products. If

businesses can simply reduce some other costs to offset the rise in the

cost in energy products and metals, they might be able to keep most of

their customers.

A major area where a manufacturer or service

provider can cut costs is in wage expense. (Note the different types of

expenses shown in Figure 5. Wages are a major type of expense for most

businesses.)

There are several ways employment costs can be cut:

- Shift jobs to lower wage countries overseas.

- Use automation to shift some human labor to labor provided by electricity.

- Pay workers less. Use “contract workers” or “adjunct faculty” or “interns” who will settle for lower wages.

If

a manufacturer decides to shift jobs to China or India, this has the

additional advantage of cutting energy costs, since these countries use a

lot of coal in their energy mix, and coal is an inexpensive fuel.

Figure

9. United States Labor Force Participation Rate by St. Louis Federal

Reserve. It is computed by dividing the number of people who are

employed or are actively looking for work by the number of potential

workers.

In fact, we see a drop in the US civilian labor

force participation rate (Figure 9) starting at approximately the same

time when energy costs and metal costs started to rise. Median

inflation-adjusted wages have tended to fall as well in this period. Low

wages can be a reason for dropping out of the labor force; it can

become too expensive to commute to work and pay day care expenses out of

meager wages.

Of course, if wages of workers are not growing and

in many cases are actually shrinking, it becomes difficult to sell as

many homes, cars, boats, and vacation cruises. These big-ticket items

create a significant share of commodity “demand.” If workers are unable

to purchase as many of these big-ticket items, demand tends to fall

below the (now-inflated) cost of producing these big-ticket items,

leading to the lower commodity prices we have seen recently.

6. We are headed in slow motion toward major defaults among commodity producers, including oil producers.

Quite

a few people imagine that if oil prices drop, or if other commodity

prices drop, there will be an immediate impact on the output of goods

and services.

Figure 10.

Instead, what happens is more of a time-lagged effect (Figure 11).

Figure 11.

Part

of the difference lies in the futures markets; companies hold contracts

that hold sale prices up for a time, but eventually (often, end of

2015) run out. Part of the difference lies in wells that have already

been drilled that keep on producing. Part of the difference lies in the

need for businesses to maintain cash flow at all costs, if the price

problem is only for a short period. Thus, they will keep parts of the

business operating if those parts produce positive cash flow on a

going-forward basis, even if they are not profitable considering all

costs.

With debt, the big concern is that the oil reserves being used as collateral for loans will drop in value, due

to the lower price of oil in the world market. The collateral value of

reserves works out to be something like (barrels of oil in reserves x

some expected price).

As long as oil is being valued at $100

barrel, the value of the collateral stays close to what was assumed when

the loan was taken out. The problem comes when low oil prices gradually

work their way through the system and bring down the value of the

collateral. This may take a year or more from the initial price drop,

because prices are averaged over as much as 12 months, to provide

stability to the calculation.

Once the value of the collateral

drops below the value of the outstanding loan, the borrowers are in big

trouble. They may need to sell some of the other assets they own, to

help pay down the loan. Or, they may end up in bankruptcy. The borrowers

certainly can’t borrow the additional money they need to keep

increasing their production.

When bankruptcy occurs, many

follow-on effects can be expected. The banks that made the loans may

find themselves in financial difficulty. The oil company may lay off

large numbers of workers. The former workers’ lack of wages may affect

other businesses in the area, such as car dealerships. The value of

homes in the area may drop, causing home mortgages to become

“underwater.” All of these effects contribute to still lower demand for

commodities of all kinds, including oil.

Because of the time lag

problem, the bankruptcy problem is hard to reverse. Oil prices need to

stay high for an extended period before lenders will be willing to lend

to oil companies again. If it takes, say, five years for oil prices to get up to a level high enough to encourage drilling again, it may take seven years before lenders are willing to lend again.

7.

Because many “baby boomers” are retiring now, we are at the beginning

of a demographic crunch that has the tendency to push demand down

further.

Many workers born in the late 1940s and in

the 1950s are retiring now. These workers tend to reduce their own

spending, and depend on government programs to pay most of their income.

Thus, the retirement of these workers tends to drive up governmental

costs at the same time it reduces demand for commodities of all kinds.

Someone

needs to pay for the goods and services used by the

retirees. Government retirement plans are rarely pre-funded, except with

the government’s own debt. Because of this, higher pension payments by

governments tend to lead to higher taxes. With higher taxes, workers

have less money left to buy homes and cars. Even with pensions, the

elderly are never a big market for homes and cars. The overall result is

that demand for homes and cars tends to stagnate or decline, holding

down the demand for commodities.

8. We are running short of options for fixing our low commodity price problem.

The

ideal solution to our low commodity price problem would be to find

substitutes that are cheap enough, and could increase in quantity

rapidly enough, to power the economy to economic growth. “Cheap enough”

would probably mean approximately $20 per barrel for a liquid oil

substitute. The price would need to be correspondingly inexpensive for

other energy products. Cheap and abundant energy products are needed

because oil consumption and energy consumption are highly correlated. If

prices are not low, consumers cannot afford them. The economy would

react as it does to inefficiency. In other words, it would react as if

too much of the output is going into intermediate products, and too

little is actually acting to expand the economy.

Figure

12. World GDP in 2010$ (from USDA) compared to World Consumption of

Energy (from BP Statistical Review of World Energy 2014)

These

substitutes would also need to be non-polluting, so that pollution

workarounds do not add to costs. These substitutes would need to work in

existing vehicles and machinery, so that we do not have to deal with

the high cost of transition to new equipment.

Clearly, none of the

potential substitutes we are looking at today come anywhere close to

meeting cost and scalability requirements. Wind and solar PV can only be

built on top of our existing fossil fuel system. All evidence is that

they raise total costs, adding to our “Increased Inefficiency” problem,

rather than fixing it. Other solutions to our current problems

seem to be debt based. If we look at recent past history, the story

seems to be something such as the following:

Besides adopting QE

starting in 2008, governments also ramped up their spending (and debt)

during the 2008-2011 period. This spending included road building, which

increased the demand for commodities directly, and unemployment

insurance payments, which indirectly increased the demand for

commodities by giving jobless people money, which they used for food and

transportation. China also ramped up its use of debt in the 2008-2009

period, building more factories and homes. The combination of QE,

China’s debt, and government debt together brought oil prices back up by

2011, although not to as high a level as in 2008 (Figure 7).

More

recently, governments have slowed their growth in spending (and debt),

realizing that they are reaching maximum prudent debt levels. China has

slowed its debt growth, as pollution from coal has become an increasing

problem, and as the need for new homes and new factories has become

saturated. Its debt ratios are also becoming very high.

QE

continues to be used by some countries, but its benefit seems to be

waning, as interest rates are already as low as they can go, and as

central banks buy up an increasing share of debt that might be used for

loan collateral. The credit generated by QE has allowed questionable

investments since the required rate of return on investments funded by

low interest rate debt is so low. Some of this debt simply recirculates

within the financial system, propping up stock prices and land prices.

Some of it has gone toward stock buy-backs. Virtually none of it has

added to commodity demand.

What we really need is more high wage jobs. Unfortunately, these jobs need to be supported by the availability of large amounts of very inexpensive energy.

It is the lack of inexpensive energy, to match the $20 per barrel oil

and very cheap coal upon which the economy has been built that is

causing our problems. We don’t really have a way to fix this.

9. It is doubtful that the prices of energy products and metals can be raised again without causing recession.

We

are not talking about simply raising oil prices. If the economy is to

grow again, demand for all commodities needs to rise to the point where

it makes sense to extract more of them. We use both energy products and

metals in making all kinds of goods and services. If the price of these

products rises, the cost of making virtually any kind of goods or

services rises.

Raising the cost of energy products and metals

leads to the problem represented by Growing Inefficiency (Figure 4). As

we saw in Point 5, wages tend to go down, rather than up, when other

costs of production rise because manufacturers try to find ways to hold

total costs down. Lower wages and higher prices are a huge

problem. This is why we are headed back into recession if prices rise

enough to enable rising long-term production of commodities, including

oil.

http://www.theenergycollective.com/gail-tverberg/2252055/nine-reasons-why-low-oil-prices-may-morph-something-much-worse

No comments:

Post a Comment