By Harris

Roen

Alternative energy became a serious market player after the turn

of the millennium. Since that time, solar, wind, smart grid and

other alternative energy stocks have experienced both strong up

and down trends. The forces at work driving these markets are

complex, counterintuitive, and sometimes mysterious. This article

looks at what has been driving the price of alternative energy

markets, and as a result, alternative energy company stocks.

Looking ahead, we will also consider what should affect the

direction of alternative energy stock prices.

Past trends in Alternative Energy Stocks

The Wilder Hill New Global Index (NEX) is a fitting proxy to

track overall alternative energy markets. This index contains

companies that “focus on generation and use of cleaner

energy, conservation and efficiency, and advancing renewable

energy generally.” The chart at right shows some of the

clear trends the alternative energy sector has had in the recent

past.

The first down channel on the chart coincides with a general

stock market slump. This drop started during the eight month

recession which began in March 2001.

By 2003, alternative energy stocks started to turn around. This

marked the beginning of a fantastic five year run, as investors

started noticing wind power and photovoltaics were becoming

economically viable alternatives to traditional electric

generation. Annualized returns in this five year period averaged a

remarkable 38%!

The Great Recession then hit in December 2007, just as

alternative energy stocks appeared to be ascending into nosebleed

territory. As a result, prices came crashing down a painful 71% in

about a year. This outstripped the distressing declines the stock

market in general had at that time.

After this crash, no clear trend emerged until the end of 2012,

when the next up-channel started. At that time, investors felt

that alternative energy stock prices better reflected the economic

realities of the underlying business, and started buying again.

There is likely another reason, though, that it took five years

for alternative energy markets to recover. Psychologically, after

getting severely burned in the crash of 2008, it took a long time

for investors to feel comfortable dipping their toes back in the

water.

Following the uptrend that went from 2012 to the beginning of

2014, there was a noteworthy giveback. The NEX fell 21% in about

nine and a half months. Much of that giveback has been regained.

It remains to be seen if the current trend will continue to be

positive, or if we have entered into a sideways market.

Do Fossil Fuel Prices Drive Alternative Energy Markets?

Are fossil fuel prices the main driver of failure or success of

green energy companies? Though this seems like a reasonable

theory, the answer, in my analysis, is that it depends.

Alternative Energy versus Oil

Most of the larger alternative energy stocks

are multinational corporations that are part of an international

economy. As a comparison, crude oil prices are good indicator of

global fossil fuel values. Oil is a worldwide commodity that can

more easily flow to markets than coal or natural gas. The latter

two fossil fuels are subject to local supplies and disruptions, so

prices can range widely by region.

Most of the larger alternative energy stocks

are multinational corporations that are part of an international

economy. As a comparison, crude oil prices are good indicator of

global fossil fuel values. Oil is a worldwide commodity that can

more easily flow to markets than coal or natural gas. The latter

two fossil fuels are subject to local supplies and disruptions, so

prices can range widely by region.

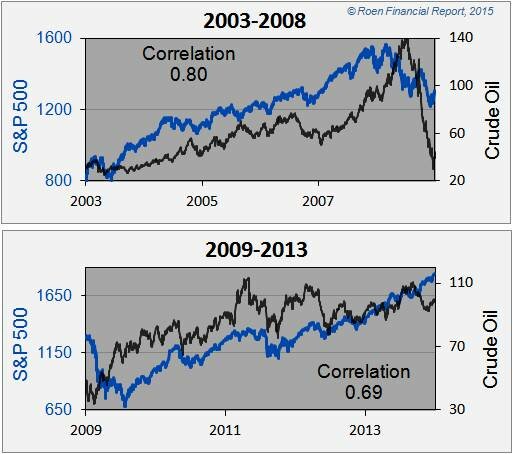

The chart at right shows crude oil (Cushing

OK spot) as compared to the NEX over two time periods. From

2001 to 2009, oil and alternative energy prices were very strongly

linked. For you math wonks, the two had a correlation coefficient

of 0.87, which is extremely significant. This makes sense, since a

rise in oil prices would mean that other energy alternatives

become more attractive. From 2010 to the present, the NEX had a

slight negative correlation to oil prices. The two markets did not

exactly go in opposite directions, but they had virtually no

corresponding movement.

A further reason for the 2002-2009 correlation

is that the economy was humming along very well at that time. This

helped fuel investor optimism that the market would continue to

grow for solar, wind, and the like. Similarly, oil became a strong

proxy for the stock market at that time, as speculators started

investing heavily in oil. They believed that as the global economy

expanded, there would be more demand for oil, thus raising the

prospects for oil prices. In essence, oil became a proxy for the

stock market.

A further reason for the 2002-2009 correlation

is that the economy was humming along very well at that time. This

helped fuel investor optimism that the market would continue to

grow for solar, wind, and the like. Similarly, oil became a strong

proxy for the stock market at that time, as speculators started

investing heavily in oil. They believed that as the global economy

expanded, there would be more demand for oil, thus raising the

prospects for oil prices. In essence, oil became a proxy for the

stock market.

The correlation between oil and the stock market remained strong

for a decade, but finally started to diverge at the end of 2013.

Since then there has been a strong negative correlation.

Oil prices are now being affected

more by supply and demand. Much of this has to do with the North

American oil and natural gas boom, which is injecting an abundance

of supply right where it is being used. This not only tips the

supply/demand equation by reducing

U.S. oil imports, but also mitigates the fear that oil

prices will skyrocket when a crisis crops up in the Middle East.

For this reason, I expect any rise in oil prices going forward

will positively affect alternative energy stocks.

Oil prices are now being affected

more by supply and demand. Much of this has to do with the North

American oil and natural gas boom, which is injecting an abundance

of supply right where it is being used. This not only tips the

supply/demand equation by reducing

U.S. oil imports, but also mitigates the fear that oil

prices will skyrocket when a crisis crops up in the Middle East.

For this reason, I expect any rise in oil prices going forward

will positively affect alternative energy stocks.Alternative Energy versus Natural Gas

Often, the decline in alternative energy electricity generators

such as wind and solar has

been attributed a drop in natural gas prices. There is a

correlation between the two, though it is not as strong as one

might think.

The charts at right show natural gas (Henry Hub

LA spot) compared to the NEX. There is a clearly a

correlation between the two, though it is somewhat weak. It is

also interesting to note that at starting around 2015, there was a

divergence between natural gas prices and the NEX.

Prospects for Alternative Energy Stocks

Though no one can tell with certainty where alternative energy

stocks will head in the future, there are factors that can shed

some light on the long-term prospects for this sector. These

include increased manufacturing efficiencies, financial

innovations and energy policy.

Efficiencies

Much of what many alternative energy companies do is similar to

tech sector stocks. As product design and production engineering

keeps improving, manufacturing efficiency can greatly help a

company’s bottom line. Whether its photovoltaics,

LED lighting

or wind

arrays, the cost of production continues to drop for green

economy companies. This trend shows no signs of abating, which

bodes well for alternative energy investors.

Financial Innovations

The alternative energy sector has profited greatly from new and

innovative financial models. Companies like SolarCity

(SCTY)

and SunPower

(SPWR)

have benefited from various financial arrangements that allow

consumers to install solar with no upfront costs. These include

lease arrangements, power buyback agreements, and securitization

of tax benefits.

Another innovative financial model to benefit alternative energy

is the advent of renewable

YieldCo’s. These are companies that bundle solar and wind

generating assets into predictable cash flows that are paid out in

dividends. This innovation allows green investors can choose

from several companies with strong yield attributes.

Investors love dividends, especially in this low interest rate

environment. Any added yield an investor can put in their

portfolios is of great value. YieldCo’s should continue to attract

investors and lead to higher stock prices.

These types of financial innovation reflect a maturing of the

alternative energy sector, which I see as a good sign. As long as

these products have strong

fiscal underpinnings, the prospects for long-term growth

remain healthy.

Energy Policy

Because of the public good that results from reduced fossil fuel

use, alternative energy has benefitted from government policies

supporting the industry. Indeed, targets and incentives remain

strong internationally, particularly in Europe

and Asia.

These regions and others continue to be serious in their

commitment to solar, wind, energy storage, efficiency and other

alternative energy strategies. Domestically, there are two

important policy developments to watch, one a carrot and one a

stick.

The first important domestic incentive is the Business

Energy Investment Tax Credit (ITC). The ITC rebates up to

30% for solar, fuel cells, wind, combined heat and power (CHP) and

geothermal. This incentive is scheduled to sunset at the end of

2016. Whether it gets renewed or not will affect the rate at which

renewable projects go forward. This will cause concern for

investors.

The second policy development is the Clean

Power Plan. These proposed rules from the EPA target

pollution reduction from power plants, and will have a vast affect

on how energy gets produced and consumed in the country.

Essentially each state has an emission target, which will force it

to find ways to reduce carbon emissions. There has been some

strong pushback from many states, especially those heavily reliant

on coal for production electricity. The rule making process will

likely take a few

years and several court cases to resolve, but if the Clean

Power Plan remains mostly intact, it will accelerate renewable

energy projects in a big way.

Conclusion

By keeping an eye to the ground on fossil fuel prices, energy

policies and other factors, investors can go far to understanding

prospects for alternative energy stocks. There will undoubtedly be

up and down swings ahead, but there are enough positives

underlying the sector that we remain bullish for the long-term.

http://www.altenergystocks.com/archives/2015/04/alternative_energy_stock_returns_past_and _future.html

No comments:

Post a Comment