There is a lot of confusion about which limit we are

reaching with respect to oil supply. There seems to be a huge amount of

“reserves,” and oil production seems to be increasing right now, so

people can’t imagine that there might be a near term problem. There are

at least three different views regarding the nature of the limit:

- Climate Change. There is no limit on oil production within the foreseeable future. Oil prices can be expected to keep rising. With higher prices, alternative fuels and higher cost extraction techniques will become available. The main concern is climate change. The only reason that oil production would drop is because we have found a way to use less oil because of climate change concerns, and choose not to extract oil that seems to be available.

- Limit Based on Geology (“Peak Oil”). In each oil field, production tends to rise for a time and then fall. Therefore, in total, world oil production will most likely begin to fall at some point, because of technological limits on extraction. In fact, this limit seems quite close at hand. High oil prices may play a role as well.

- Oil Prices Don’t Rise High Enough. We need high oil prices to keep oil extraction up, but as we reach diminishing returns with respect to oil extraction, oil prices don’t rise high enough to keep extraction at the required level. If oil prices do rise very high, there are feedback loops that lead to more recession and job layoffs and less “demand for oil” (really, oil affordability) among potential purchasers of oil. One major cut-off on oil supply is inadequate funds for reinvestment, because of low oil prices.

Why “Oil Prices Don’t Rise High Enough” Is the Real Limit

In my view, our real concern should be the third item above, “Oil Prices Don’t Rise High Enough.”

Because

of diminishing returns, the cost of oil extraction keeps rising. It is

hard for oil prices to increase enough to provide an adequate profit for

producers. In fact, oil prices already seem to be too low. Oil

companies have begun returning money to stockholders in increased

dividends, rather than investing in projects which are likely to be

unprofitable at current oil prices. See Oil companies rein in spending to save cash for dividends. If

our need for investment dollars is escalating because of diminishing

returns in oil extraction, but oil companies are reining in spending for

investments because they don’t think they can make an adequate return

at current oil prices, this does not bode well for future oil

extraction.

A related problem is debt limits

for oil companies. If cash flow does not provide sufficient funds for

investment, increased debt can be used to make up the difference. The

problem is that credit limits are soon reached, leading to a need to cut

back on new projects. This is particularly a concern where high cost

investment is concerned, such as oil from shale formations. A rise in

interest rates would also be a problem, because it would raise costs,

leading to a higher required oil price for profitability. The debt

problem affects high priced oil investments in other countries as well. OGX, the second largest oil company in Brazil, recently filed for bankruptcy, after it ran up too much debt.

National

oil companies don’t explain that they are finding it hard to generate

enough cash flow for further investment. They also don’t explain that

they are having a hard time finding sites to drill that will be

profitable at current prices. Instead, we are seeing more countries

with national oil companies looking for outside investors, including Brazil and Mexico.

Brazil received only one bid, and that for the minimum amount,

indicating that oil companies making the bids do not have high

confidence that investment will be profitable, either. Meanwhile,

newspapers spin the story in a totally misleading way, such as, Mexico Gears Up for an Oil Boom of Its Own.

US natural gas is another product with a similar problem: the price is not high enough to justify new production, especially for shale gas producers. The huge resource that some say is there is simply too expensive to extract at current prices. Would-be natural gas producers cannot tell us this. Instead, we find a recent quote in the Wall Street Journal saying:

“We are not dealing with an era of scarcity, we are dealing with a situation of abundance,” Ken Cohen, Exxon’s vice president of public and government affairs, said in an interview. “We need to rethink the regulatory scheme and the statutory scheme on the books.”

Cohen

could explain that without natural gas exports, there is no way the

natural gas price will rise high enough for Exxon-Mobil to extract the

resource at a profit. Without exports, Exxon Mobil will lose money on

the extraction, or more likely, will have to leave the natural gas in

the ground. With low prices, the huge resource that Obama has talked

about is simply a myth–the prices need to be higher. Of course, no one

tells us the real story–it seems better to let people think that the

issue is too much natural gas, not that it can’t be extracted at the

current price. The stories offered to the news media are simply ways to

convince us that exports make sense. Readers are not aware how much

stories can be “spun” to make the current situation sound quite

different from what it really is.

What Goes Wrong with “Climate Change” and “Limit Based on Geology” Views

The Illusion of Reserves. Oil and gas reserves may seem to be “be there,” but a lot of conditions need to be in place for them to actually

be extracted. Clearly, the price needs to be high enough, both for

current extraction and to fund new investment. Other conditions need to

be in place as well: Debt needs to be available, and it needs to be

available at a sufficiently low rate of interest to keep costs down.

There needs to be political stability in the country in question.

Something as simple as a continuation of the uprisings associated with

the Arab Spring of 2010 could lead to the inability to extract reserves

that seem to be present. Other requirements include availability of

water for fracking and the availability of skilled workers and drilling

rigs.

In the past, we have been far enough away from limits that

issues such as these have not been a big problem. But as we get closer

to limits and stretch our capabilities, these become more of a problem.

Right now, availability of debt at low interest rates is a particularly

important issue, as is the need for adequate oil company

profitability–things that are easy to overlook.

Wrong Economic Views Leading to Wrong Oil Views. Economists

have put together economic models based on a world without limits. A

world without limits is the easy approach, because mathematical

relationships are much simpler in a world without limits: a relationship

which held in 1800 is expected to hold in 1970 or in 2050. A world

without limits never offends politicians, because growth always seems to

be possible, meaning a never-ending supply of jobs and of goods and

services for constituents. A model without limits produces the simple

relationships that we are accustomed to, such as “Inadequate supply will

lead to a rise in price, and this in turn will tend to create greater

supply or substitutes.” Unfortunately, these models omit many important

variables and thus are inadequate representations of the world we live

in today.

In a world with

limits, there are feedback loops that cause high oil prices to lead to

lower wages and more unemployment in oil importing countries. Thus

“demand” can’t keep rising, because workers can’t afford the higher oil

prices. Oil prices stagnate at a level that is too low to maintain

adequate investment. High oil prices also feed back into slower economic

growth and a need for ultra-low interest rates to raise demand for

high-priced goods such as cars and homes.

When prices

remain in the $100 barrel range, they are still high enough to damage

the economy. Businesses are not much damaged, because they have ways

they can work around higher oil prices, especially if interest rates are

low. Most of the ways businesses can work around high oil prices

involve reducing wages to US workers–for example, outsourcing production

to a lower cost country, or cutting the pay of workers, or laying off

workers to match lower demand for goods. (Lower demand for goods tends

to occur when oil prices rise, and businesses raise their prices to

reflect the higher oil costs.)

Workers are still affected by costs

in the $100 barrel range, and so are governments. Governments must pay

out higher benefits than in the past, to keep the economy afloat. They

must also keep interest rates very low, to try to keep demand for homes

and cars as high as possible. The

situation becomes very unstable, however, because very low interest

rates depend on Quantitative Easing, and it does not appear to be

possible to continue Quantitative Easing forever. Thus, interest rates

will need to rise. Such a rise in interest rates is likely to push the

country back into recession, because taxes will need to be higher (to

cover the government’s higher debt costs) and because monthly payments

on homes and new car purchases will tend to rise. The limit on oil

production then becomes something very remote from geology–something

like, “How long can interest rates remain low?” or “How long can we make

our current economy function?”

The Interconnected Nature of the Economy. In my last post, I talked about the economy being a complex adaptive system.

It is built from many parts (many businesses, laws, consumers,

traditions, built infrastructure). It can operate within a range of

conditions, but beyond that range it is subject to collapse. An

ecosystem is a complex adaptive system. So is a human being, or any

other kind of animal. Animals die when their complex adaptive system

moves out of its range.

It is this interconnectedness of the

economy that leads to the strange situation where something very remote

from the real problem (oil limits) can lead to a collapse. Thus, it can

be a rise in interest rates or a political collapse that ultimately

brings the system down. The path of the downslope can be very different

from what a person might expect, based on the naive view that the

problems will simply relate to reduced supply of oil.

A Case Study of the Collapse of the Former Soviet Union

The

Soviet Union was major oil exporter and a military rival of the United

States in the 1950s through 1980s. It also was the center of a huge

economic system, involving many other countries. One thing that bound

the countries together was the use of communism as its method of

government; another was trade among countries. In effect, the group of

communist countries had their own complex adaptive system. Things seemed

to go fine for many years, but then in December 1991, the central

government of the Soviet Union was dissolved, leaving the individual

republics that made up the Former Soviet Union (FSU) on their own.

While

there are many theories as to what all caused the collapse, it seems to

me that low prices of oil played a major role. The reason why low oil

prices are important is because in an oil exporting country, such as the

FSU, oil export revenues represent a major part of government funding.

If oil prices drop too low, there is a double problem: (1) it becomes

unprofitable to drill new wells, so production drops and, (2) the

revenue that is collected on existing wells drops too low. The problem

is then a huge financial problem–not too different from the

financial problem the US and many of the big oil importing countries are

experiencing today.

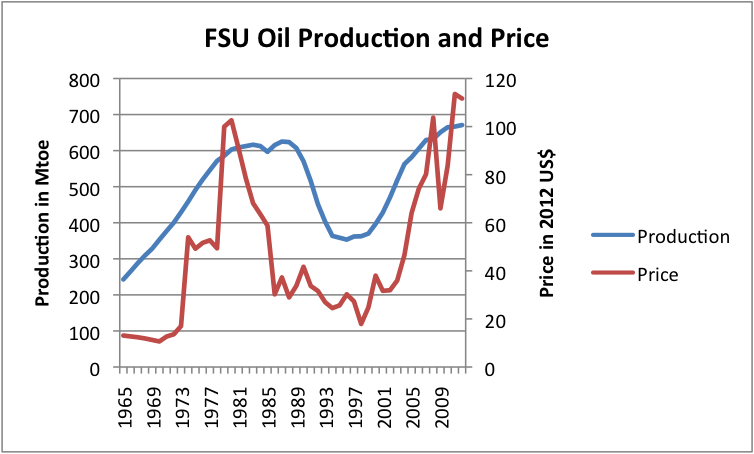

Figure 1. Oil production and price of the Former Soviet Union, based on BP Statistical Review of World Energy 2013.

In

this particular situation, oil prices (in inflation adjusted prices)

hit a peak in 1980. Once oil prices hit a peak, FSU oil production very

much flattened. There was a continued small rise until 1983, but without

the very high prices available until 1980, aggressive investment in new

oil extraction dropped back.

Not only did FSU oil production

flatten, but FSU oil consumption also flattened, not long after oil

production stopped rising (Figure 2). This flattening helped maintain

exports and the taxes that could be collected on these exports.

Figure 2. Former Soviet Union Oil Production and Consumption, based on BP Statistical Review of World Energy, 2013.

Even

though total exports were close to flat in the 1980s (difference

between consumption and production), there were some countries where

exports that were rising–for example North Korea, shown in Figure 4.

This mean that oil exports for some allies needed to be cut back as

early as 1981. Figure 3 shows the trend in oil consumption for some of

FSU’s allies.

Figure 3. Oil consumption as a percentage of 1980 consumption for Hungary, Romania, and Bulgaria, based on EIA data.

A

person can see that oil consumption dropped off slowly at first, and

increased around 1990. All of these countries saw their oil consumption

drop by at least 40% by 2000. Bulgaria saw is oil consumption drop by

65% to 70%.

The FSU exported oil to other countries as well. Two

countries that we often hear about, Cuba and North Korea, were not

affected in the 1980s (Figure 4). In fact, Cuba’s oil consumption never

seems to have been severely affected. (It is possible that exports of

manufactured goods from the FSU dropped, however.) Cuba’s drop-off in

oil consumption since 2005 may be price-related.

Figure 4. Oil consumption as a percentage of 1980 oil consumption for Cuba and North Korea, based on EIA data.

North

Korea’s oil consumption continued growing until 1991. Its drop-off was

then very severe–a total of an 83% reduction between 1991 and 2010. In

most of the countries where oil consumption dropped, consumption of

other fossil fuels dropped as well, but generally not by as large

percentages. North Korea experienced nearly a 50% drop in other fuel

(mostly coal) consumption by 1998, but this has since somewhat reversed.

By

1991, the FSU was in poor financial condition, partly because of the

low oil prices, and partly because its oil exports had started dropping.

FSU’s oil production left its plateau and started dropping about 1988

(Figure 2). The actual drop in FSU oil production meant that oil

consumption for the FSU needed to drop as well–a big problem because

industry depended upon this oil. The break-up of the FSU was a solution

to these problems because (1) it eliminated the cost of the extra layer

of government and (2) it made it easier to shift oil consumption among

the member republics, so that those republics that produced more oil

could keep it for their own use, rather than sending it to republics

which did not produce oil. This shortchanged non-oil producing

republics, such as the Ukraine and Belarus.

If we look at oil

consumption for a few of the republics that were previously part of the

FSU, we see that oil consumption was fairly flat, then dropped off

quickly, after 1991.

Figure

5. Oil consumption as a percentage of 1985 oil production for Russia,

the Ukraine, and Belarus, based on BP Statistical Review of World Energy

2013.

By 1996 (only 5 years after 1991), oil

consumption had dropped by 78% for the Ukraine, by 61% for Belarus, and

by “only” 47% for Russia, which is an oil-producing state. At least

part of the reason for the fast drop off was the fact that in the years

immediately after 1991, oil production for the FSU dropped by about 10%

per year, necessitating a quick drop off in consumption, especially if

the country was to continue to make some money from exports. The 10%

drop-off in oil production suggests that the decline in oil production

was more than would be expected from geological decline alone. If the

decline were for geological reasons only, without new drilling, one

might the expect the drop off to be in the 4% to 6% range.

When

oil consumption dropped greatly, population tended to decline (Figure

6). The decline started earliest in the countries where the oil

consumption drop was earliest (Hungary, Romania, and Bulgaria). The

steepest drop-offs in population occur in the Ukraine and Bulgaria–the

countries with the largest percentage drops in oil consumption.

Figure 6. Population as percent of 1985 population, for selected countries, based on EIA data.

Some

of the population drop is from emigration. Some of it is from poorer

health conditions. For example, Russia used to provide potable water for

its citizens, but it no longer does. Some is from conditions such as

alcoholism. I haven’t shown the population change for North Korea. It

actually continued to increase, but at a much lower rate of growth than

previously. Cuba’s population has begun to fall since 2005.

GDP growth for the countries shown has tended to lag behind world economic growth (Figure 7).

Figure 7. GDP compared to world GDP – Change since 1985, based on USDA Real GDP data.

Nearly all of the countries listed above have had financial problems, at different times.

Belarus’s

GDP seems to be doing better than the rest on Figure 7. Belarus, like

the Ukraine, is a pipeline transit country for Russia. In Belarus,

natural gas consumption has increased, even as oil consumption has

decreased. This increase is likely helping the country industrialize.

Inflation occurred at the rate of 51.9% in 2012 according to the CIA World Fact Book. This high inflation rate may be distorting indications.

Conclusion

We

can’t know exactly what path our economy will follow in the future. I

expect, though, that the path of the FSU and its trading partners is

closer to the path we will be following than most forecasts we hear

today. Most of us haven’t followed the FSU story closely, because we

wrote off most of their problems to deficiencies of communism, without

realizing that there was a major oil component as well.

The FSU

situation may, in fact, be better that what the Industrialized West is

facing in the next few years. The FSU had the rest of the world to

support it, offering investment capital and new models for development.

Oil production for Russia was able to rebound when oil prices rose again

in the early 2000s. As situations around the world decline, it will be

harder to “bootstrap.”

One of the things that hampered the

recovery of the FSU was the fact that the communist economic model

proved not to be competitive with the capitalistic model. In a way, the

situation we are facing today is not all that different, except that our

challenge this time is competition from Asian economies that we have

not had to compete with until the early 2000s.

Asian economies have several cost advantages relative to the Industrialized West:

(1)

Asian competitor countries are generally warmer than the industrialized

West. Because of this, Asian workers can live more comfortably in

flimsy homes. They also don’t need much salary to cover heating and can

more easily commute by bicycle. It is often possible to produce two

crops a year, making productivity of land and of farmers higher than it

otherwise would be. In other words, Asian competitor countries have an

energy subsidy from the sun that the Industrialized West does not.

(2) Asian competitors are often willing to ignore pollution problems, reducing their costs relative to the West.

(3)

Asian competitors generally depend on coal to a greater extent than we

do, keeping their costs down, relative to countries that use

higher-priced fuels.

(4) Asian competitors are less generous with employee benefits such as health care and pensions, also holding costs down.

Economists,

through their wholehearted endorsement of globalization, have pushed

industrialized countries into a competitive situation which we are

certain to lose. While oil prices tend to push wages down, competition

with Asian countries makes the downward push on wages even greater.

These lower wages are part of what are pushing us toward collapse.

To

solve our problems, economists have proposed a shift toward renewable

energy and the implementation of carbon taxes. Unless these changes are

done in a way that actually reduces costs, these “solutions” are likely

to make us even less competitive with low-cost competitors such as those

in Asia. Thus, they are likely to push us toward collapse more quickly.

To

support this position, economists point to climate change models based

on the view that the burning of fossil fuels will increase greatly in

the decades again. In fact, if collapse occurs in the next few years in

the Industrialized West, carbon emissions are likely to fall quickly.

Because of the interconnectedness of the world system, the rest of the

world will likely also encounter collapse in not many more years, and

their carbon emissions are likely to fall quickly, as well. Even the

“Peak Oil” emissions that are used in climate change models are way too

high, relative to what seems likely to be the case.

If I am right

about collapse being a possibility for the Industrialized West, then our

problem will be that we as nations become so poor that we can no longer

find goods to trade with Asian countries. Most of our goods will not be

competitive as exports, and we won’t be able to simply add more debt to

rectify the situation. Thus, we will become unable to buy many goods we

depend on, including computers and replacement parts for wind turbines.

Breakups

of many types are possible. The European Union may cease to operate in

the way it does today. The International Monetary Fund is likely to

cease operating in the way it does today, because of the collapse of

many of its members who provide funding. The US will be subject to

strains of the type that lead to break up. If nothing else, oil

producing states will want to withdraw, so that they are not, in effect,

subsidizing the rest of the US economy.

It is unfortunate that

economists are tied to their hopelessly out-of-date economic models.

Part of the problem is that the story of “collapse around the corner”

doesn’t sell well. The alternate story economists have come up with

really isn’t right, but it is pleasing to the many who benefit from

subsidies for renewables, and it makes politicians look like they are

doing something. The specter of climate change in the distance gives an

excuse to cut back oil use, among other things, so has at least some

theoretical benefit.

It is unfortunate, however, that we cannot

look at the real problem. Unless we can understand the problem as it

really is, it is impossible to find solutions that might actually be

helpful.

http://theenergycollective.com/gail-tverberg/319501/th-real-oil-extraction-limit-and-how-it-affects-downslope

No comments:

Post a Comment