In my view, oil and gas resource limits are major contributors to the conflict in Syria. This is happening in several ways:

1. Syria is an oil exporter that is in increasingly perilous financial condition because of depleting oil resources. When

oil production is increasing, it can help an oil exporter in two ways:

(a) part of the of the oil supply can be used internally, to grow more

food and to support increased industry, and (b) exports of oil can be

used to provide revenue for governmental programs such as food

subsidies, education, and building highways. Syria’s population grew

from 8.8 million in 1980 to 22.8 million in 2012, at least in part

because of the wealth available from oil extraction.

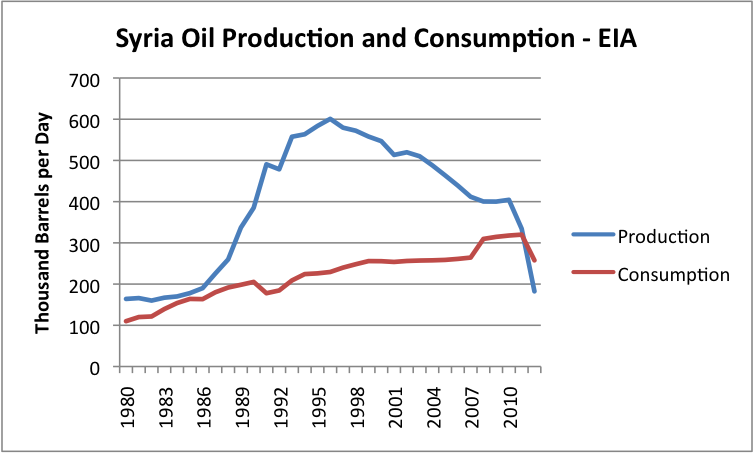

Figure 1. Syria’s oil production and consumption, based on data of the US Energy Information Administration.

Now

Syria’s oil production is dropping. The drop between 1996 and 2010

reflects primarily the effect of depletion. The especially steep drop in

the last two years reflects the disruption of civil war and

international sanctions, in addition to the effect of depletion.

When

oil exports drop, the government finds itself suddenly less able to pay

for programs that people have been expecting, such as food subsidies

and new irrigation programs to support agriculture. If revenue from oil

exports is sufficient, desalination of sea water is even a possibility. In Syria, wheat prices doubled between 2010 and 2011,

for a combination of reasons, including drought and a cutback in

subsidies. When basic commodities become too high priced, citizens tend

to become very unhappy with the status quo. Civil war is not unlikely.

Thus, oil depletion is likely a significant contributor to the current

unrest.

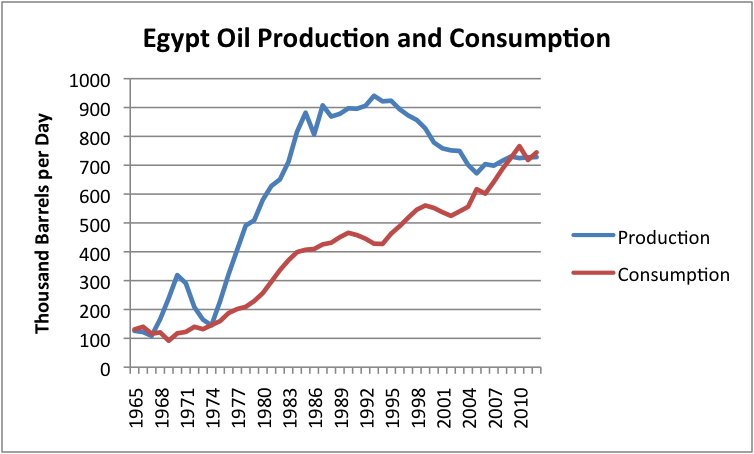

Egypt has many Similarities to Syria

Egypt

is another example of an oil exporter whose oil production has dropped

because of geological decline. Its chart of oil production and

consumption (Figure 2) looks very much like Syria’s (Figure 1).

Figure 2. Egypt’s oil production and consumption, based on BP’s 2013 Statistical Review of World Energy data.

Egypt

is actually doing a little better than Syria. One of the things that

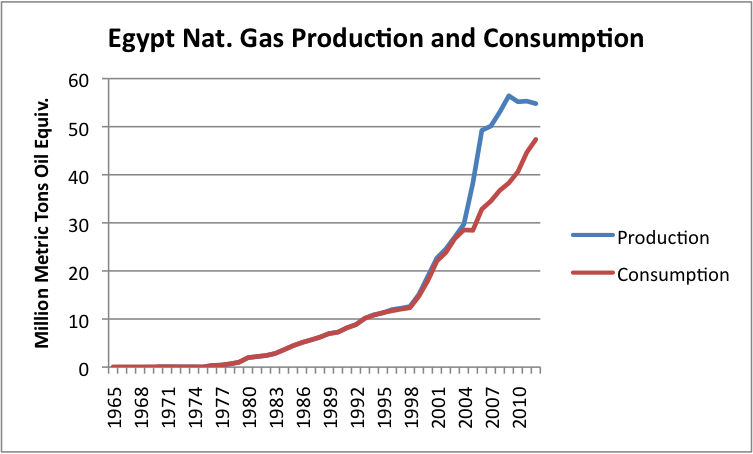

has helped Egypt is its natural gas production, because it has been

another source of export revenue. Unfortunately, Egypt’s natural gas

production suddenly flattened starting in 2009, again because of

depletion (Figure 3).

Figure 3. Egypt natural gas production and consumption based on BP 2013 Statistical Review of World Energy.

As

Egypt started losing oil supplies, it was able to keep its own energy

consumption growing (to keep up with growing population) by rapidly

cutting back on exported natural gas (even though it had contracts in

place to sell some of the this natural gas). Part of this cutback was to its pipeline customers,

namely Israel, Lebanon, and Syria. Of course, this left Egypt with less

foreign revenue to fund subsidies, education, and many other programs,

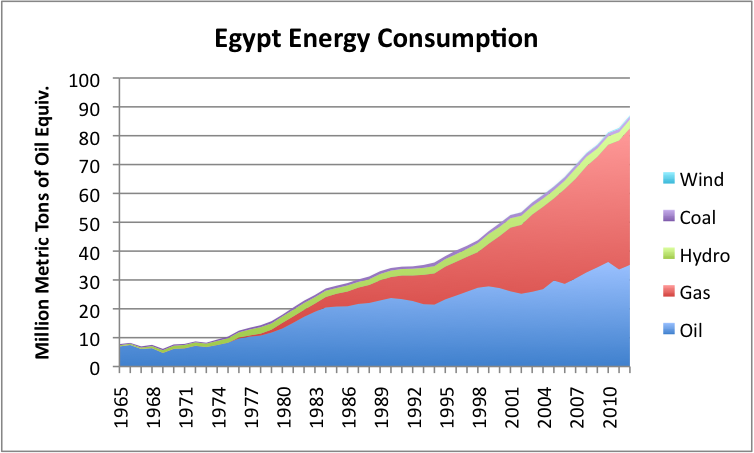

but Egypt’s own energy consumption (Figure 4) was able to keep growing,

helping agriculture and industry to function as normal.

Figure 4. Egypt’s energy consumption by source, based on BP 2013 Statistical Review of World Energy.

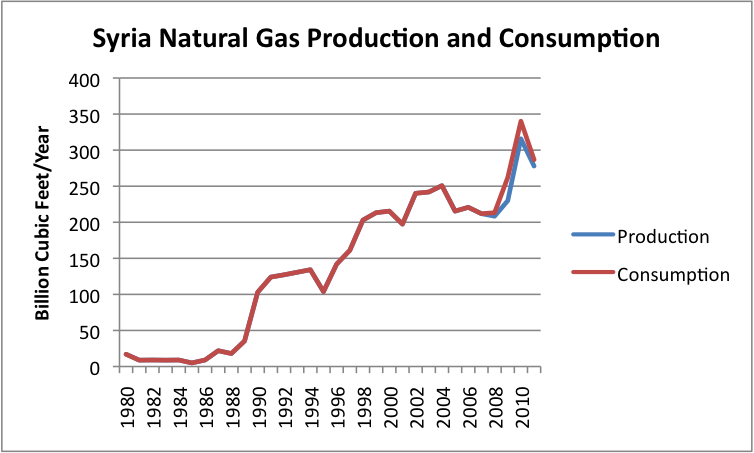

Syria,

on the other hand, was consuming all of the natural gas it produced. In

fact, is was importing a little gas from Egypt, so it had no exports it

could cut back on. In fact, Egypt’s cutback worked the wrong way from

Syria’s perspective–it lost a small amount of natural gas imports from

Egypt.

Figure 5. Syria Natural Gas production and consumption, based on data of the US Energy Information Administration.

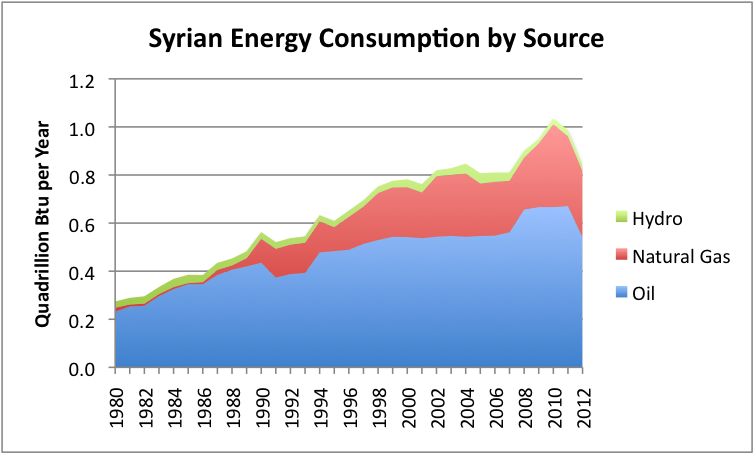

As a result, Syria found its energy consumption decreasing (Figure 6), even as population continued to rise.

Figure 6. Syria Energy Consumption by Source, based on EIA data.

At least part of the decline in Syria’s energy consumption occurred because of damage to oil and gas pipelines and to electrical transmission equipment. According to the CIA Fact Book,

Syria’s industrial production shrank by 36% in 2012. Thus, geological

depletion and the civil war that grew out of inadequate resources both

contributed to the drop in energy consumption.

Going forward, this

tendency toward civil disorder is likely to get worse, whether or not

the US decides to attack. The underlying issue in Figure 1 is depletion.

Population remains high. Even if damage to pipelines and transmission

lines get fixed, the depletion issue will continue, and the population

will need to be fed.

2. Economic sanctions, to the extent

they have an affect, can be expected to act similarly to resource

depletion and increase the tendency toward civil disorder.

Syria has been operating under economic sanctions from the US since 2004.

To the extent that these had an effect, one would expect that they

would reduce economic activity, and thus energy consumption. It is hard

to see a significant change in energy use patterns in the years

immediately after 2004, from the charts provided.

Many other countries have added sanctions since hostilities broke out in 2011. It

is difficult to tell how much effect the 2011 sanctions have actually

had. It is possible that they contributed to Syria’s drop in energy

consumption. It is also possible the civil disorder together with

depletion explain the recent drop in oil production and consumption.

Even with sanctions, Syria continues to participate in international trade. According to the EIA, Syria continues to trade with Russia, Iran, Iraq, Malaysia, and Venezuela. Other sources mention China (here and here) as a trading partner with Syria. North Korea is also mentioned as being a trading partner, especially in the area of chemical weapons.

3. Oil pipelines from Iraq through Syria would be helpful if Iraq is to greatly ramp up its oil output in the next few years.

The

United States has an interest in getting oil production from Iraq

ramped up, in the hope that world oil production can continue to rise.

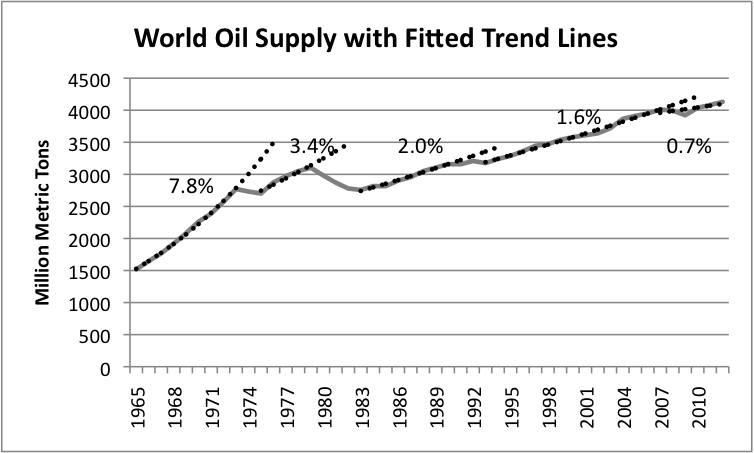

World oil production has been increasingly flat, even taking into

account liquid substitutes and new sources, such as biofuel and new US

tight oil production.

7. Growth in world oil supply, with fitted trend lines, based on BP 2013 Statistical Review of World Energy.

One

of the limits in ramping up Iraqi oil extraction is the limited amount

of infrastructure available for exporting oil from Iraq. If pipelines

through Syria could be added, this might alleviate part of the problem

in getting oil to international markets. According to the EIA,

One particular project proposes to build two oil pipelines (and one for natural gas) that would send Iraqi crude to the Mediterranean coast in Syria, and from there to international markets. The first of the proposed pipelines would send heavier crudes from northern Iraq and have a capacity of 1.5 million bbl/d. The second pipeline would send lighter grades from southern Iraqi fields, and would follow the same route as the former Haditha-Banias pipeline; the second section is scheduled to have a 1.25 million bbl/d capacity.

4. The

possibility of natural gas pipelines through Syria to alleviate

potential shortages in Europe and elsewhere is contentious.

Russia

currently is a major exporter of natural gas to Europe. It would like

to keep natural gas prices as high as possible because of the high cost

of its natural gas extraction, and because of the high cost of building

new pipelines. Russia does not necessarily welcome new natural gas

production from, for example, Qatar or Israel, carried by pipeline

through Syria. Such new supply might reduce natural gas prices in

Europe, either because of oversupply or because the other natural gas

sources have a lower cost of extraction and transport.

If new

pipelines are built through Syria, there are several countries that

might theoretically ship natural gas through such pipelines, and there

is considerable rivalry among these countries. For example, Israel and

Iran are rivals as to which country might export natural gas to Europe.

Also, as noted above, there is a possibility that natural gas from Iraq

could be exported through Syria to the international market, if suitable

pipelines were built. There is even theoretically a possibility that

natural gas from Turkmenistan could be exported by pipeline through

Iran, Iraq and Syria, cutting out Russia (and the profits it receives in

buying, transporting and selling this gas).

It should be noted

that even though many countries have their sights set on exporting

natural gas to Europe and other parts of the world that need natural

gas, it is not at all clear that this additional transport of natural

gas will work out as planned. We have known for a long time about a

large amount of “stranded” natural gas–gas that is theoretically

available, but it simply too expensive to extract and ship to locations

where it might be purchased. The limits on how much natural gas will be

consumed are financial–how much can consumers really afford.

The

affordability issue is clear if we think about a family in India, living

on $2 a day, deciding whether to burn animal dung or compressed natural

gas for cooking. If the price of natural gas is high, the family in

India will choose to burn dung. A similar issue arises for a pensioner

in the UK, deciding to what temperature to heat his home. It also arises

for an electric power plant in Germany, deciding whether to burn natural gas or coal.

If the cost of natural gas is too high, demand is likely to shift to

cheaper fuels, or to disappear through alternative behavior–for example,

wearing long underwear to keep warm in winter, instead of heating homes

as warmly as today.

5. Need for America to prove its might, to maintain the US dollar’s reserve currency status.

Without

the reserve currency status of the US dollar, America cannot continue

to run a big balance of payment deficit importing large quantities of

oil. This is important, because the world’s total oil supply is not

growing much (Figure 7), regardless of price. If America is forced to

consume less, more oil will be available for the rest of the world.

Conclusion

Because

of its oil depletion, Syria will remain a problem country, regardless

of whether the US decides to intervene militarily. Removing Assad as

leader of Syria cannot be expected to solve Syria’s problems. Even if

oil deletion were not the major issue, US’s recent experience in Libya

suggests that removing a leader does not guarantee future stability.

Associated Press reports this week, Libya’s oil exports plunge as problems escalate.

Some

may argue that Syria has other gas and oil that it can exploit, and

because of this, its depletion problems are only temporary. In

particular, the EIA report on Syria

notes that there are both shale oil resources in Syria and natural gas

resources offshore that Syria might develop. In my view, there are

several reasons that this optimism is unwarranted. As a practical

matter, even if there were peace and plenty of investment capital,

developing these resources would take several years. During this period,

other countries would need to donate enough resources to keep the

population pacified. Can this really be done, especially if other

countries are reaching limits themselves?

Furthermore, it is not

at all clear that extraction of oil from shale can really be developed

profitably. No one outside North America has yet figured out how to do

so. The US has laws and pipeline infrastructure that are different from

elsewhere that help make shale development possible at reasonable cost.

Available credit and low interest rates are also helpful. The US also

has abundant water resources, and population that is not too dense, so

that fracking is less of an issue than it would be elsewhere. A recent Wall Street Journal article talks about the difficulty China is having trying to extract hydrocarbons from shale.

There

is also the question I mentioned above with respect to the economic

feasibility of new natural gas resources. If the cost is too high, the

cost may simply be too high for buyers. Furthermore, if buyers find a

need to cut back on other expenditures to purchase gas products (or for

that matter, high-priced oil products), they are likely to cut back in

the purchase of other discretionary items. Layoffs are likely to occur

in discretionary sectors, leading to recession and reduced demand

through fewer jobs. Thus, one way or another, a reduction in demand is

likely to occur.

Egypt and Syria are not the only countries in the

area with oil depletion problems. Yemen’s oil chart of oil production

and exports (Figure 8) looks very much like that of Syria and Egypt.

Figure 8. Yemen oil production and consumption, based on US Energy Information Administration data.

Saudi Arabia may even be reaching limits on its extraction capability. It recently is reporting refocusing on unconventional resources,

something it would not do if conventional oil were performing well.

Saudi Arabia is also using a greater number of drilling rigs, reported

to be necessary because of the increasing difficulty of extracting oil from mature fields.

If

oil depletion is becoming an increasing problem, I am afraid we can

expect increasing conflict in the Middle East, regardless of whether the

US chooses to intervene in Syria because of increased oil depletion. A

shortfall in one country can ripple to the next country, and on to the

next country, as exports are reduced, and as civil unrest spreads.

It

is easy to blame bad leaders for the problem, or a bad form of

government. Much of the problem, however, is simply not having enough

oil resources to go around for the size of population the world has

today. We can kid ourselves about additional oil and natural gas

resources being available, but these very much depend on the ability of

buyers to pay higher prices, without excessive recessionary impacts.

http://theenergycollective.com/gail-tverberg/271176/oil-and-gas-limits-underly-syria-s-conflict

No comments:

Post a Comment